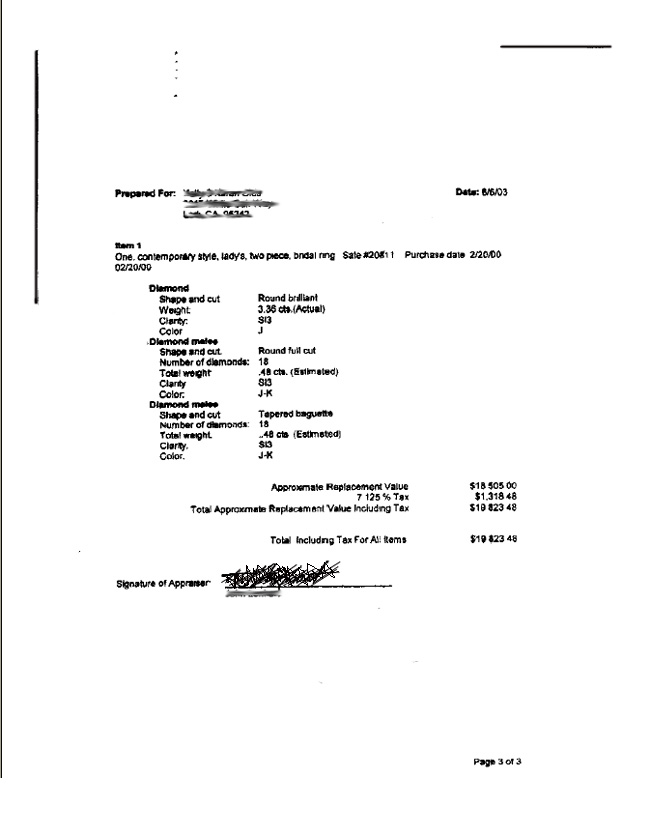

Can you recognize a good appraisal?

Test your wits on some real-world appraisals, typical of those received

every day by agents and underwriters

and used by adjusters to settle claims.

Question: Which of these are good appraisals?

Answer: NONE of them!

And that usually leads to settlement overpayments.

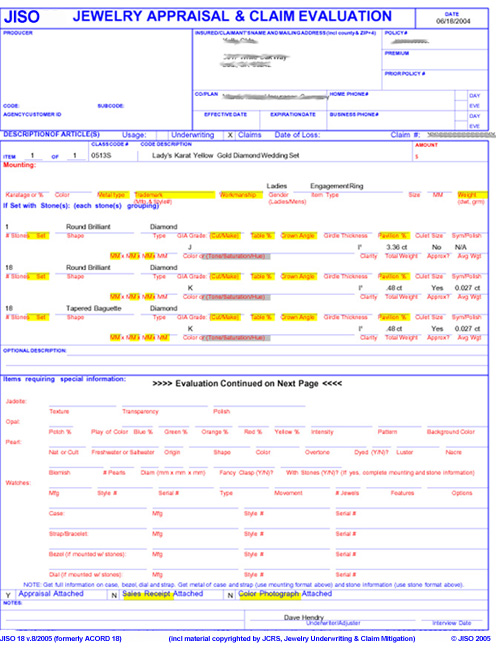

Let's have a closer look. Below, you can see each appraisal scored for completeness using JISO 18, Jewelry Appraisal & Claim Evaluation.

Highlighting on JISO 18 shows missing information that is crucial to accurate valuation.

Appraisal 1

|

|

Appraisal 1 |

Appraisal 1 |

The orderly presentation of information is misleading. This appraisal doesn't discuss mounting at all, doesn't even say what metal is used.

The words next to "shape and cut" (round brilliant, round full, tapered baguette) are all terms for shape only. Cut information, describing the stone's precise geometric proportions (table %, crown angle, pavilion % — highlighted on JISO 18), is simply not given. Cut is one of the "4 Cs" of gems, along with color, clarity and carat weight. In diamonds, cut accounts for fully half the gem's value. A reliable valuation cannot be made without this information.

A little fudging appears in the description of clarity as SI-3 ("slightly imperfect-3") There is no such designation in standard GIA grading. This grade actually translates to I-1 ("imperfect-1"), which means inclusions are visible to the naked eye.

Appraisal 2

|

|

Appraisal 2 |

Appraisal 2 |

This succinct appraisal leaves out crucial cut and mounting information.

Notice also the paragraph that follows the appraiser's signature. It begins by certifying the truth and correctness of the appraisal, but then undercuts that assurance by stating, "We assume no liability with respect to any action that may be taken on the basis of this appraisal." It may as well say: Don't base your claim settlement on this appraisal and valuation.

A professional appraiser should, in fact, stand behind his word and expertise. For a more trustworthy warrantee of truth, see the paragraph above the appraiser's signature on the JISO 78/79 Jewelry Appraisal, which is the insurance industry's standard.

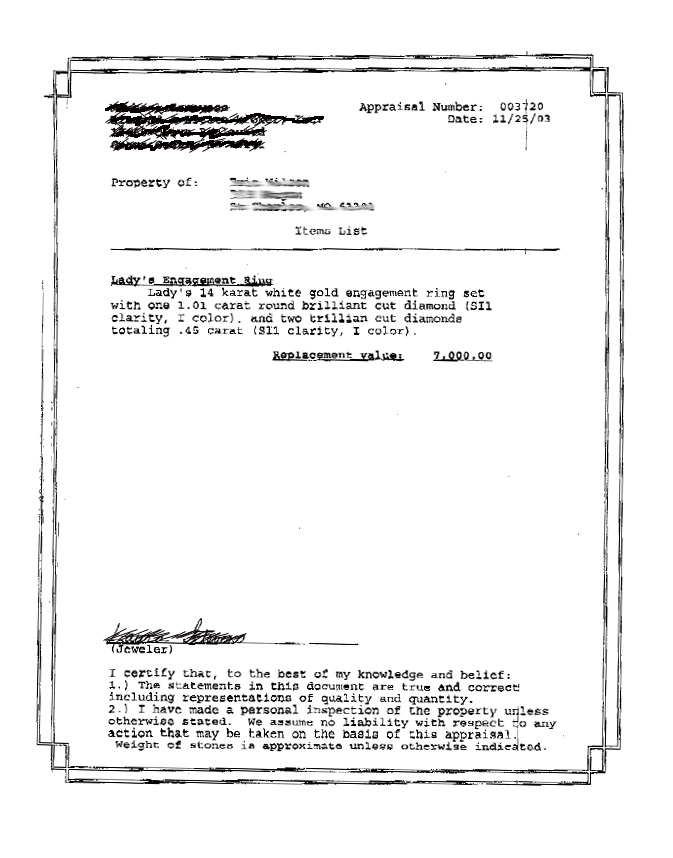

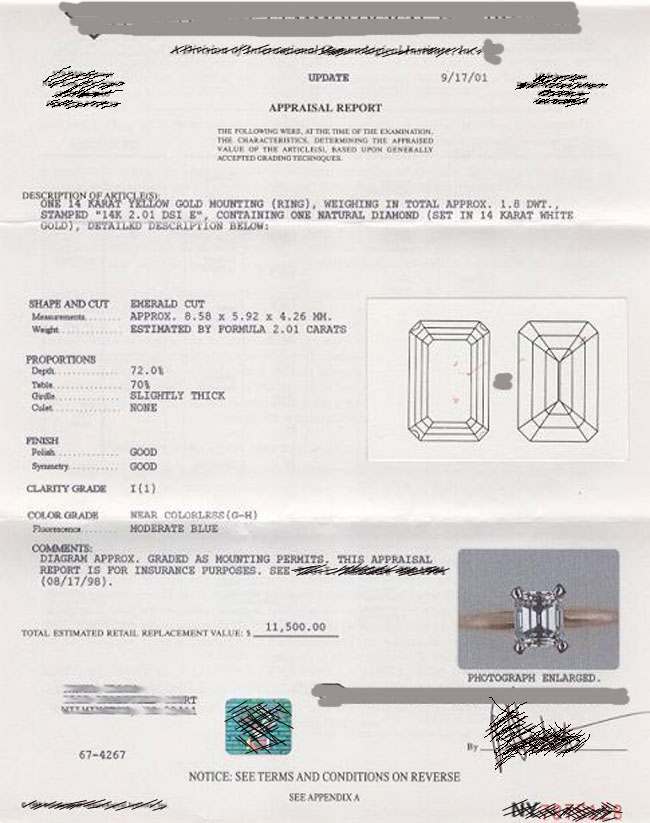

Appraisal 3

|

|

Appraisal 3 |

Appraisal 3 |

In addition to all the missing information highlighted on JISO 18, this one isn't even called an appraisal—and the title says it all. The no-liability clause, above the appraiser's signature, emphasizes again that this is not really an important document. It is, after all, just for insurance.

Appraisal 4

|

|

Appraisal 4 |

Appraisal 4 |

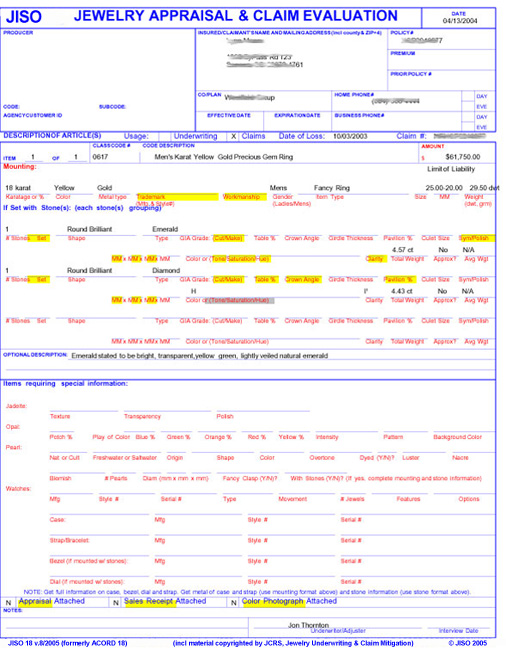

This is a so-called "narrative" appraisal, where all information is packed into a dense paragraph. JISO 18 shows that information is missing on cut, setting and mounting.

Since this jewelry was the subject of a damage claim, rather than a total loss, other appraisal problems became apparent. The appraisal describes the emerald as yellow green, but examination of the damaged stone showed it to be bluish green. In addition, tone and saturation were omitted. These discrepancies are not trivial. The major determinant for an emerald's value is its color, and the descriptive language for color stones is standardized and quite precise.

Based on the replacement cost submitted by the original seller/appraiser, the insurer settled the claim for $49,000. A jewelry insurance expert, consulted afterwards to deal with the salvage, found that the emerald could have been replaced for $8,279.

The original appraisal was grossly inflated. In settling the claim the adjuster made two mistakes: 1) he accepted the appraisal at face value, and 2) he accepted the selling jeweler's cost of replacement. If, instead, he had consulted a disinterested jewelry professional to verify valuation before settling the claim, he could have avoided the $40,000 overpayment.

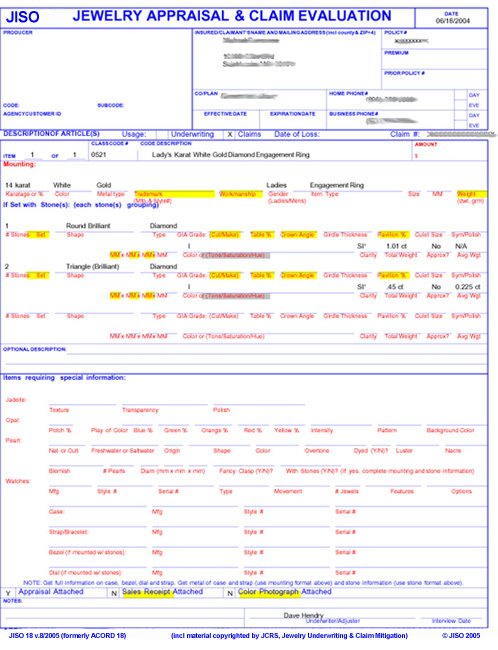

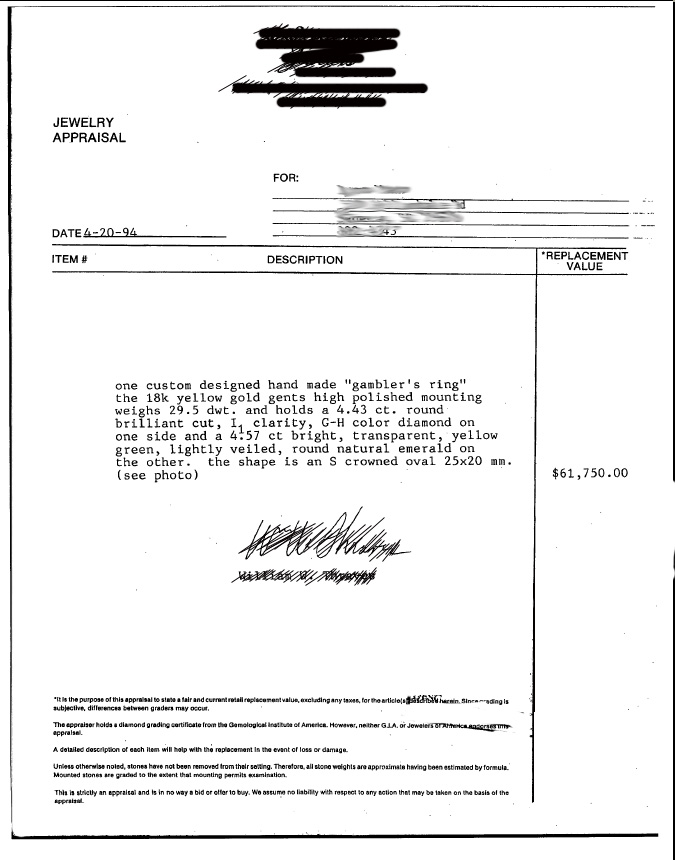

Appraisal 5

|

|

Appraisal 5 |

Appraisal 5 |

This is a formal and impressive-looking document, patterned after the Diamond Reports produced by such respected labs as the Gemological Institute of America. This, however, is NOT from a respected lab. It leaves out the same crucial information omitted on handwritten appraisals from mom-and-pop jewelers.

To cap it off, the valuation is also grossly inflated. Appraisals with inflated valuations are often used as sales tools, to convince purchasers they are getting bargains.

Summary

- NONE of these appraisals has complete information on cut.

- NONE of these appraisals has complete information on mounting.

- NONE gives the manufacturer, style number or workmanship,

and one even omits weight. - NONE describes the setting.

- And only one of them was prepared by a Graduate Gemologist.

What It All Means

Customers count on insurers to properly insure their property. Relying on an inadequate appraisal, like one of those above, is a setup for problems in the event of a claim.

The price of replacement is based on specific qualities of the jewelry. Since the adjuster cannot supply information that is missing from the appraisal, the jeweler must make it up in order to give a quote. Thus, the settlement is based on guesswork. If the settlement is too high, the insurer has overpaid; if it’s too low, the customer is dissatisfied—and that dissatisfaction may affect the client’s other business with the agent or insurer.

The JISO Solution

Both unfortunate outcomes—carrier overpayment and customer

dissatisfaction—are avoided with a JISO 78/79 Jewelry Appraisal.

This standardized appraisal lists all qualities that distinguish the jewelry

from any other and all details that are necessary for valuation. This means

no guesswork when it comes to claims. The replacing jeweler has a complete

description of the jewelry he is quoting to replace. And the adjuster can

comparison shop for quotes, confident that all jewelers are quoting on the

same exact piece.

If a policyholder submits an appraisal other than JISO 78/79, the agent

can use JISO 18, Jewelry Appraisal and Claim Evaluation,

to determine the adequacy of the submittted appraisal. It contains the minimal

information necessary to determine jewelry value. Information lacking on

the submitted appraisal will be obvious.

Agents can use JISO 18 to discuss with policyholders how jewelry is insured and, if necessary, encourage them to get a more complete appraisal (preferably on JISO 78/79). They can point out that a detailed appraisal insures that the jewelry is properly insured and that the premiums are appropriate. In case of a claim, the appraisal verifies that the settlement is fair and the replacement accurate. This kind of conversation assures clients that the agent is looking out for their interests.

In short: satisfied customers and no overpayments.